Banking

Here’s How Cash App For Teens And Families Can Help Your Teen Learn To Manage Their Money Safely

**Teen-Friendly Banking: Cash App Introduces Safe Money Management for Families**

“`html

What’s Happening?

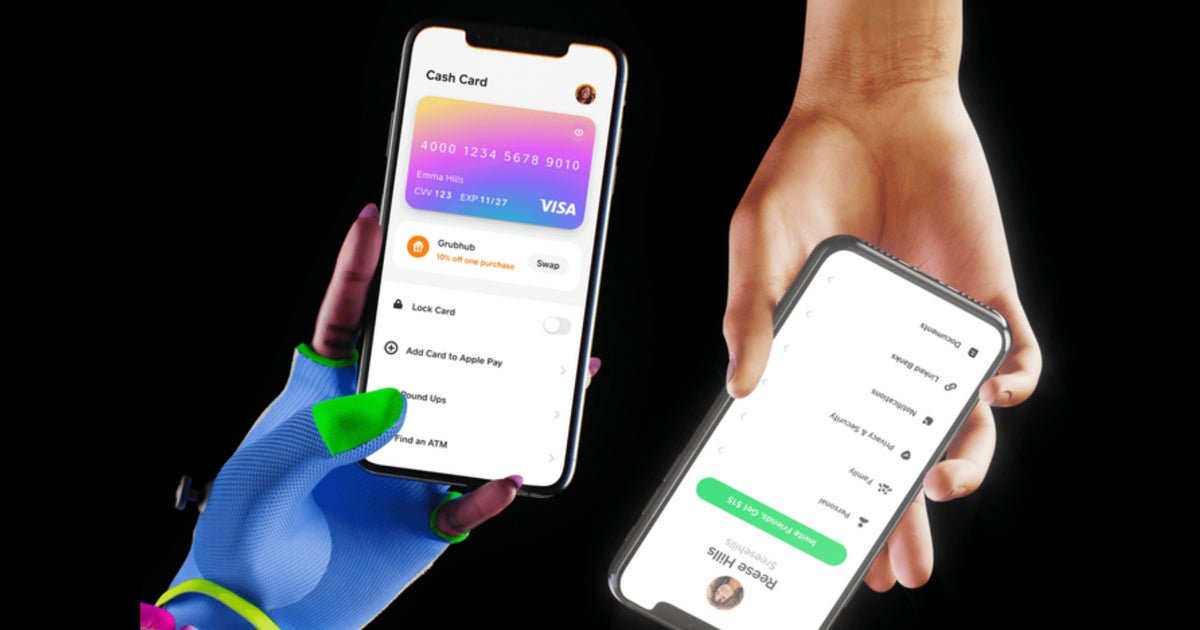

Cash App has launched a new feature designed to empower teens with financial literacy while offering parents peace of mind. Cash App Families provides a secure, educational banking experience tailored for teenagers aged 13 to 17, blending hands-on financial management with parental oversight

Where Is It Happening?

This service is available nationwide within the United States, accessible via the Cash App mobile platform.

When Did It Take Place?

The launch of Cash App Families coincides with the growing demand for financial education tools for young people, with no specific debut date mentioned, indicating an ongoing rollout.

How Is It Unfolding?

- Teens gain access to a dedicated Cash App account with features like spending control and automated allowance features.

- Parents can monitor activity, set spending limits, and receive real-time alerts.

- The platform includes educational resources to help teens understand budgeting, saving, and responsible spending.

- Teens can use their accounts for spending, saving, and learning without the risks of traditional banking.

- Cash App plans to expand features based on user feedback and evolving financial education needs.

Quick Breakdown

- Brands Cash App Families as a secure, educational tool for teens.

- Parents retain control over spending and transactions.

- Available to US users aged 13 to 17.

- Aims to bridge the gap between financial independence and parental supervision.

- Includes budgeting tools and personalized spending insights.

Key Takeaways

Cash App Families is a balanced solution for teens eager to manage their finances and parents striving to guide them safely. By offering a dedicated platform with real-time monitoring and educational tools, it fosters financial literacy from an early age. This initiative meets the need for secure, guided financial experiences for young people, helping them build healthy money habits before they enter adulthood.

Early financial education is crucial, and Cash App Families is a step in the right direction. However, parents shouldn’t rely solely on apps—personal financial discussions remain invaluable.

– Sarah Jenkins, Financial Education Advocate

Final Thought

**Cash App Families is a game-changer for teens eager to learn financial responsibility. With a user-friendly interface and robust parental controls, it offers a safe way to explore money management. By integrating education and real-world experience, this tool could set the foundation for a lifetime of smart financial decisions. It’s a smart move for families looking to balance independence with guidance.

“`

Trade’s Biggest Threat Isn’t Tariffs-It’s Uncertainty

Exclusive: Top South Korea official says policy institutions to lead on $350 billion US fund, watching FX